Tillis Targets Debanking

A new bill responding to debanking has appeared. After months of deliberations, Senator Thom Tillis (R‑NC) introduced the Ensuring Fair Access to Banking Act. The 90-page bill aims to create “a strong federal fair access standard to [ensure] that no American or lawful business is denied banking services for political or ideological reasons.” Although the bill repeats some of the missteps found in Senator Kevin Cramer’s (R‑ND) Fair Access to Banking Act, the bill also offers some notable improvements.

What the Ensuring Fair Access to Banking Act Gets Right

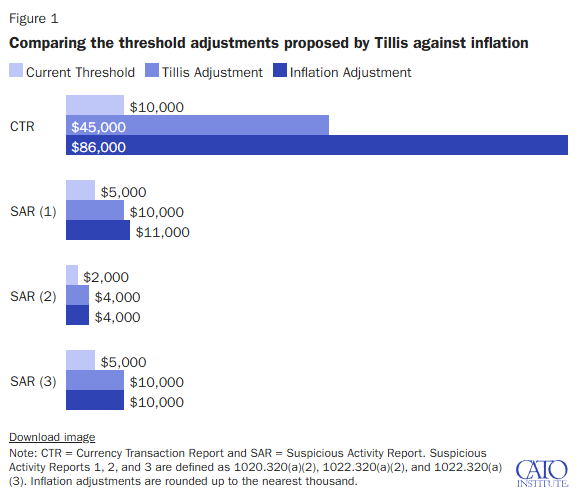

Starting with what it gets right, the bill would make some improvements that would ease the pressure of governmental debanking. For example, there is an “inflation adjustment” for currency transaction reports (CTRs) and suspicious activity reports (SARs). These reports can be filed for fairly mundane reasons, but they end up labeling customers as being a high risk. Once that happens, all of the incentives push banks to close the accounts. Removing (or at least lessening) these incentives could go a long way in reducing debanking.

However, while the SAR thresholds are adjusted appropriately, the proposed CTR threshold falls short of the proper adjustment (Figure 1).

Unfortunately, the bill is also missing adjustments for the reports on foreign bank and financial accounts (FBARs), reports of international transportation of currency or monetary instruments (CMIRs), and Form 8300 reports. These reports are not filed as often as CTRs and SARs, but they are important to correct, nonetheless.

Unfortunately, the bill is also missing adjustments for the reports on foreign bank and financial accounts (FBARs), reports of international transportation of currency or monetary instruments (CMIRs), and Form 8300 reports. These reports are not filed as often as CTRs and SARs, but they are important to correct, nonetheless.

The next thing the bill gets right is officially ending the practice of reputational risk regulation. This section is similar to Senator Tim Scott’s (R‑SC) Financial Integrity and Regulation Management (FIRM) Act. Reputational risk was one of the core tools used in Operation Choke Point, so it’s good to see this tool would finally be taken off the books. And while it’s true that regulators have slowly pulled the practice and President Trump issued an executive order to stop it as well, future administrations could easily reverse course. Legislation, on the other hand, would be much harder to undo.

Speaking of regulators and accountability, the bill would also add some much-needed transparency by making Federal Reserve banks subject to Freedom of Information Act (FOIA) requests. Due to their quasi-governmental status, the regional Federal Reserve Banks are not subject to FOIA requests like your typical regulator. The regional banks did adopt a FOIA-like process for transparency in 2024, but the bill would make the process more formal.

What the Ensuring Fair Access to Banking Act Gets Wrong

With that said, the bill does make a few mistakes. Most notably, the Ensuring Fair Access to Banking Act is based on a questionable premise. The idea that conservatives are suffering from widespread discrimination from bankers has become increasingly popular in recent years. The problem, however, is finding concrete cases to support this idea. Some people have had bad experiences, but few (if any) have had evidence to prove banks closed their accounts because of their political or religious preferences.

The only case cited by name in the bill’s press release was that of President Donald Trump. However, what wasn’t mentioned was that President Trump was under both criminal and civil investigations at the time. Although the President has claimed he was a victim of political discrimination, it simply cannot go ignored that his accounts were closed after people entered the Capitol on January 6, 2021 to protest his election loss. At the time, government officials were repeatedly labeling Trump and his supporters as terrorists.

This timeline is relevant because banks and other financial institutions have long been deputized as law enforcement in the fight against illicit finance. So, these institutions are held liable should they be caught providing services to people engaged in criminal activities. In other words, the legal system has placed every incentive on banks to debank someone should things go awry or become uncertain.

That brings us to the second issue: the bill would do little to remedy the problems with the Bank Secrecy Act regime (aka the regime responsible for deputizing banks as law enforcement) that incentivize banks to sever relationships with suspicious customers. As mentioned earlier, the bill would reduce the level of surveillance by adjusting reporting thresholds. However, Section 2(a)(6) of the bill states that it is acceptable to debank a customer if there is a concern that the customer has violated the law. In fact, it specifically points to the Bank Secrecy Act as an acceptable reason to debank a customer. To be clear, the Bank Secrecy Act is not the only federal statute leading banks to debank customers, but it is a leading cause.

The third issue is in how the bill decides what banks are allowed to do (Section 2(a)(5)). The bill says banks would be allowed to maximize profits, protect their stability, ensure compliance with legal and regulatory requirements, protect employees, and enforce contracts. However, at the same time, the bill says banks would not be allowed to “obtain a benefit, or avoid a harm, imposed by a constituency of the covered financial institution with the goal of getting the covered financial institution to engage in activity that would be prohibited under law.” In other words, if customers are protesting outside and boycotting the institution for something that may be deemed political, the business is not allowed to respond.

It’s possible that this “anti-protest” section was motivated by cases like JPMorgan Chase responding to protestors when it announced it would no longer finance private prisons and detention centers. What isn’t clear, however, is why this signal should be prohibited or how this prohibition would work in practice. Protesting provides valuable information to businesses and politicians, alike. Furthermore, this restriction puts businesses in a bind. Businesses should not be prohibited from changing course in response to a protest over their practices if that protest results in falling sales or otherwise persuades the business owners.

That brings us back to the first problem: identifying political discrimination. In practice, it will be difficult to define political discrimination when politics can run through so many facets of our lives. Until that can be better defined, this bill risks creating a maze of red tape.

Conclusion

In the end, Senator Tillis’s proposal might be 75 pages longer, but its foundation remains akin to Senator Kevin Cramer’s (R‑ND) Fair Access to Banking Act. Senator Tillis and his office certainly put some long hours into crafting the bill (the file name hints that what we see is the 23rd version). However, the proposed legislation would still further restrict the financial system and limit financial freedom in pursuit of a problem that hasn’t yet been properly diagnosed. In doing so, the legislators risk misidentifying the tools needed to solve the problem of debanking.

A better option is for Congress to limit its focus to governmental debanking. Reform the Bank Secrecy Act, prohibit the regulation of reputational risk, provide customers with more transparency, and leave it at that. Pushing banks toward becoming utilities risks creating a bigger mess than we already have. Luckily, Senator Tillis already has some of the main pieces in hand to achieve this goal.

Write a comment