Who Is Paying the Trump Tariffs?

WARNING: TODAY’S POST WILL BE EVEN WONKIER THAN USUAL

Until recently the question of who pays tariffs wasn’t controversial among economists. The overwhelming consensus was that under normal circumstances tariffs — taxes on imported goods — are passed on to consumers in the form of higher prices. There are caveats and exceptions to this consensus, but these caveats are well understood and for the most part don’t apply to the tariffs imposed by the Trump 47 administration.

Once tariffs became a centerpiece of Trump’s economic policy, however, views about their impact became politicized, and Trump supporters were obliged to echo his claim that foreigners, not U.S. consumers, bear the tariff burden. There was a slightly comical demonstration of this politicization during a recent House Financial Services Committee hearing, when Scott Bessent was asked whether, before joining the Trump administration, he had sent a letter to hedge fund investors declaring that “tariffs are inflationary.” At first, Bessent denied having written that. Confronted with proof that he had, he declared that he had been mistaken.

But who is, in fact, paying the Trump tariffs? Two reports released last week — the Congressional Budget Office’s latest report on the budget and economic outlook, and a study released by the Federal Reserve Bank of New York — both concluded that the tariffs are overwhelmingly being borne by U.S. households and firms. But Friday’s report on consumer prices showed fairly low inflation, rather than a big price spike from tariffs.

So are Trump officials right? Are studies concluding that Americans, not foreigners, are paying the tariffs wrong?

No and no. The evidence that foreigners aren’t paying the tariffs, which means that Americans are, is rock-solid. And the seemingly mild impact on measured inflation (the qualifier “measured” is important) isn’t a mystery once you do the math. Conventional economic analysis says that the tariffs should have pushed consumer prices around 1 percent higher than they would otherwise have been. Parsing the data to isolate the tariffs’ effect suggests that they have in fact raised prices by something close to that amount.

But I understand why the seeming contradictions between economic reports are confusing. So I thought I would postpone my next primer on the Federal Reserve and write today about who is paying the Trump tariffs.

Beyond the paywall, I’ll address the following:

1. What economic theory says about tariffs and prices

2. The evidence that foreigners aren’t paying the Trump tariffs

3. Why we shouldn’t have expected consumer prices to soar

4. Estimating the effect of tariffs on consumer prices

5. Are there still big price hikes ahead?

What economic theory says about tariffs and prices

Tariffs are taxes. Specifically, they are excise taxes, taxes levied on the sale of particular goods or services. The U.S. federal government imposes many other excise taxes, for example on the sale of airline tickets — 7.5 percent of the fare — and gasoline — 18.4 cents per gallon. In addition, state governments also impose a number of excise taxes, for example on cigarette sales.

Tariffs are excise taxes levied on the domestic sale of goods produced abroad. The principle of how these taxes work should be the same as the principles we apply to other excise taxes — the basic economics doesn’t change simply because tariffed goods cross a border. And when economists — or, for that matter, anti-tax advocates — estimate the burden of taxes, they normally assume that excise taxes are passed on to consumers in the form of higher prices. There’s no reason to believe that the price effects of taxes on the sale of goods produced abroad are any different.

Now, in practice excise taxes sometimes lead to cuts in sellers’ prices, and therefore don’t fall completely on consumers. Here’s why: by raising prices to consumers, excise taxes induce those consumers to buy less of the goods being taxed. And reduced demand for their products can induce sellers to shave a few percent off their prices. The size of this effect depends on how easy it is for sellers to reduce production or divert sales to markets where they don’t face excise taxes. (For readers who’ve taken economics, I’m talking about the elasticity of supply.)

We would, however, expect this effect to be small when it comes to U.S. tariffs. Why? Because although the U.S. has a huge economy and is a very big market, we’re still a relatively small part of the world economy as a whole. In 2024 the United States only accounted for 13 percent of total world imports. This means that foreign companies selling into the U.S. market are likely to respond to tariffs mostly by diverting their sales to other markets rather than by slashing prices. In fact, the EU has experienced a surge of Chinese imports as Chinese exporters re-directed goods that would previously have gone to the US.

OK, one more complication: Nations that impose tariffs often see their currencies rise, and a stronger dollar would, other things equal, lead to lower import prices. However, the dollar has declined, not risen, over the past year. Why this has happened is an interesting story, but not one we need to go into now.

The bottom line is that conventional economic analysis predicts that U.S. consumers, not foreign producers, will pay the bulk of U.S. tariffs. Is this what has actually happened?

The data show that foreigners aren’t paying the Trump tariffs

The U.S. Bureau of Labor Statistics collects data on import prices — the prices paid for goods purchased from abroad at their point of entry into the United States, that is, before payment of tariffs. The study just released by the New York Fed, carried out by Mary Amiti, Chris Flanagan, Sebastian Heise, and David E. Weinstein, uses these prices to estimate the “incidence” of the Trump tariffs — who paid them. The authors explain:

Suppose foreign exporters charge $100 for a good, and the importing country decides to levy a 25 percent tariff on it. If the foreign price remains unchanged at $100, the duty paid is $25, increasing the import price to $125. In this case, the tariff incidence falls entirely on the importer; in other words, there is 100 percent pass-through from tariffs to import prices, and therefore on U.S. consumers and firms.

In contrast, the exporter might lower its price in order to avoid losing market share. If foreign exporters respond to the tariff by lowering their price to $80 (i.e., $100 divided by 1.25), the price paid by importers will remain $100 (with $20 in duties paid to the government). In this case, 100 percent of the tariff incidence falls on foreign exporters, who now receive \(20 less for the same good; in other words, there is zero pass-through from the tariff since the import price is unchanged. So what do the data actually look like? Amiti et al calculate two measures of the increase in tariffs since January 2025 (I’ll explain the difference between the measures shortly): s_!66GW!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F92dd2155-1d27-4fde-aa05-8b44b796bdd2_1018x820.png)

Chart 1 Source: Amiti et al

To prevent a 10 percent tariff hike from translating into higher consumer prices, import prices — the prices that foreign exporters receive — would have to have fallen by about 9 percent. A quick look tells us that we haven’t seen anything like that:

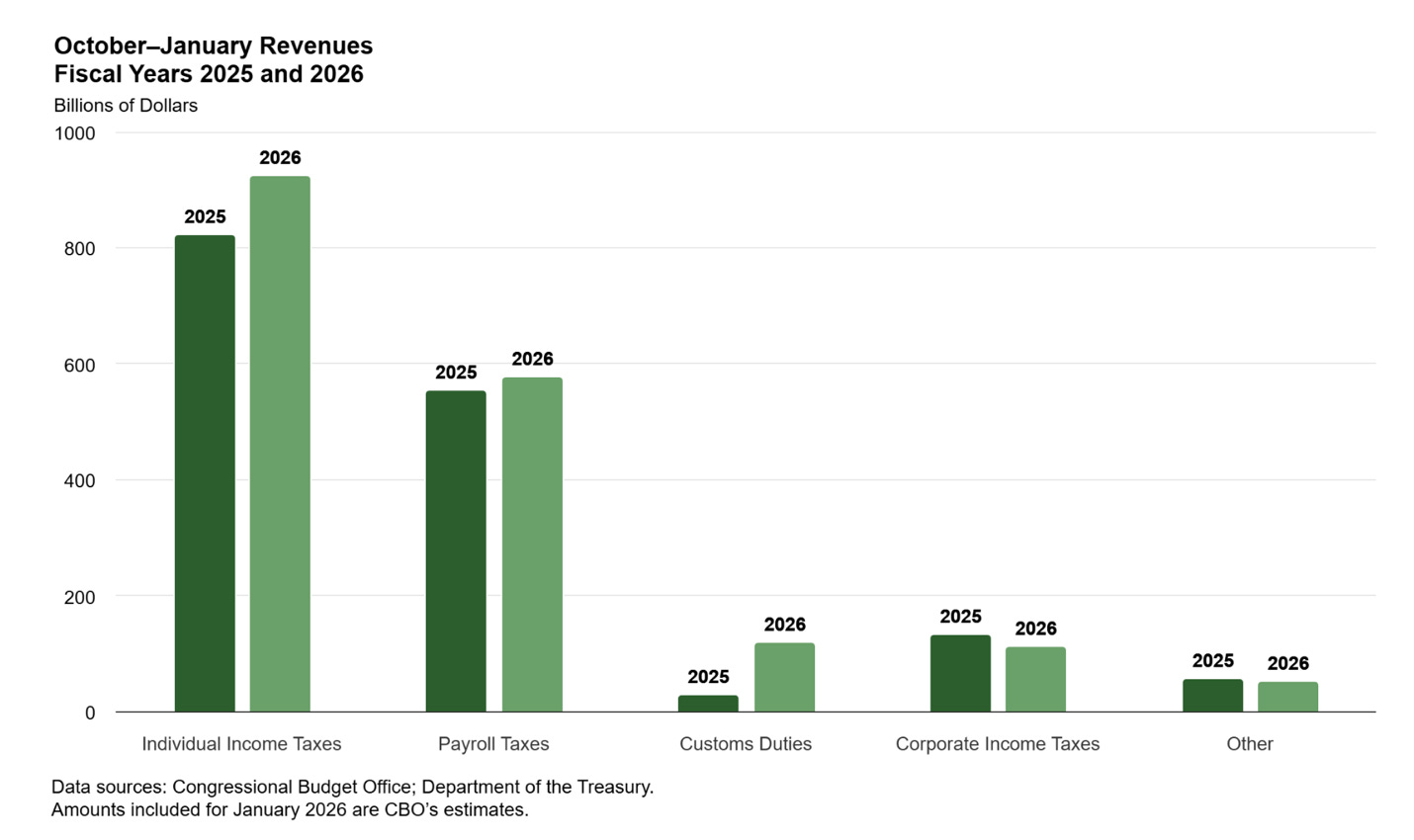

Chart 4 Source: Congressional Budget Office

Notice how small customs duties under Trump 47 are compared with income and payroll tax revenue. This serves to puncture the administration’s hype about tariffs as a revenue gusher.

We can estimate the size of the tax imposed by the tariffs relative to the size of the economy. Tariff receipts were about $90 billion higher in the last four months than in the corresponding months a year ago, or $270 billion at an annual rate. GDP in the third quarter of 2025 was \(31 trillion at an annual rate. So the tax hike was 0.27/31 = 0.87 percent of GDP. One might expect consumer prices to rise by slightly more than the direct tax effect. For example, in the [steel industry](https://www.argusmedia.com/en/news-and-insights/latest-market-news/2769786-viewpoint-us-steel-tariffs-cause-scrap-supply-glut), domestic producers raised their own prices in response to higher imported steel prices. But this happens only when domestic producers compete directly with imports. Many of the Trump tariffs have hit imports in industries in which there is no significant domestic production, such as apparel. The [Yale Budget Lab’s model](https://budgetlab.yale.edu/research/state-us-tariffs-january-19-2026) predicts a 1.2 percent rise in consumer prices as a result of current tariffs (although I’m not sure whether this model fully accounts for the gap between announced and effective tariff rates). Overall, a reasonable estimate of how much tariffs “should” have raised prices is in the vicinity of 1 percent. How does that compare with actual experience? *Estimating the effects of tariffs on consumer prices* Let’s be frank: A quick look at the Consumer Price Index — still the most widely cited measure of inflation — does not show any obvious impact of tariffs. Economists overwhelmingly try to judge inflation trends by looking at “core” inflation, which excludes volatile food and energy prices. This measure was declining steadily before the Trump tariffs, and has continued that decline (to limit clutter, I’m only showing data for successive Januaries): s_!NLzq!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fc172f1b7-aa86-41d4-8cef-3c8aa3c99220_1240x830.png)

Chart 5 Source: Bureau of Labor Statistics

Why can’t we see any effect of tariffs? Let me say right away that no, the Trump administration isn’t cooking the books. I’m not saying that they wouldn’t do so if they could, or that they won’t try in the future. But the process of producing monthly inflation reports involves a large number of professional civil servants, and we would know if that process had been corrupted. Not happening yet.

However, there is one known issue that is distorting recent inflation numbers. Due to the government shutdown last fall, the BLS was unable to collect data for two months. And for technical reasons involving the bureau’s methodology, those two missing months are still distorting one-year inflation rates, causing an understatement of price increases, especially for shelter.

There’s a general principle here that goes beyond current political disputes. I’ve been economisting for half a century (yikes). Over those years I have repeatedly encountered data that seem to contradict conventional economic analysis. In most — not all — cases, however, the problem turned out to be with the data, not conventional analysis. So if you see data that seem to say that the consensus among economists is all wrong, you should be suspicious of the data. This is especially true if the data tell you something you want to hear — if, for example, you are a Trump supporter who wants to believe that tariffs don’t raise prices.

So how can we cross-check the low inflation number the BLS just reported? One way is to look at another number. The Federal Reserve deemphasizes the CPI, preferring the Personal Consumption Expenditures price index, which is similar and relies on some of the same underlying data, but is different in detail, among other things placing a lower weight on shelter.

Unfortunately, PCE data comes in later than CPI, and we don’t yet have the numbers either for December or January. However, multiple economists produce “nowcasts” of PCE, estimates of what the number will be once reported. These estimates are closely clustered around 3, so that’s what I put in Chart 6:

Chart 8 Source: HBS Pricing Lab

Their answer is … 1 percent, right in line with what conventional economic analysis predicts.

My overall take on how tariffs have affected consumer prices runs as follows: Conventional economics predicts that tariff increases on the scale we’ve seen should have a significant but not huge effect on consumer prices — a bump to inflation, not a runaway surge. Tariffs aren’t the only thing happening to prices, so the effect of tariffs is muddied by other factors, including measurement issues resulting from the government shutdown.

But if we focus our inquiry to reduce the noise, it becomes clear that tariffs haven’t been borne by foreigners and have, for the most part, been passed on to consumers. There’s a widespread perception that the limited effect of tariffs on inflation presents a puzzle for conventional economic analysis, but this puzzle evaporates on close observation.

This leaves one final question: How much tariff-driven inflation is still in the pipeline?

Are there still big price hikes ahead?

Serious economists I follow are unanimous in accepting what CBO and Amiti et al say: The failure of import prices to fall shows that foreigners have not borne the cost of the Trump tariffs, which have therefore fallen on U.S. households and businesses. There is, however, a widespread perception that tariffs have not yet had as much effect as expected on consumer prices, seemingly implying that businesses have been absorbing tariff costs. Since we can’t expect that to go on indefinitely, this might imply substantial tariff-driven inflation still to come once businesses pass the costs on.

If I’m right, however, this is a mostly false alarm. A careful look at the evidence says that tariffs mostly have already been passed on to consumers. There may be some price increases still to come, but they are at most a fraction of 1 percent on the overall cost of living.

My guess is that the analysis in this post will leave a number of readers unhappy. Readers who want to see Donald Trump vindicated — do any such people read this Substack? — won’t like my conclusion that he was wrong and conventional economists were right. Readers who want to see disaster looming won’t like my conclusion that the worst impact of tariffs has probably already happened.

But the truth is that in practice the Trump tariffs have been a smaller story, at least in macroeconomic terms, than either their proponents or many of their opponents believe. As I have been arguing for some time, the crackdown on immigration and the pogroms against immigrants already here are a bigger economic story, even in the short run and especially in the long run.

s_!2mex!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Ffaf4273e-738d-4fad-9090-d0b88a6187ac_926x416.png](https://substackcdn.com/image/fetch/\(s_!qPTR!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F62216bd9-24d6-439c-b994-49a7c27928e7_800x450.png)

Chart 2

The measure that I use for import prices excludes petroleum because the price of oil fluctuates wildly for reasons that have nothing to do with tariff policy — e.g., who we’re bombing this week. The prices of non-oil imports shot up during the supply-chain snarls of 2021-2022, then fell. Since the massive tariff hikes of April 2025, the prices of imports (excluding oil) have gone up, not down.

Amiti et al do a much more careful assessment, breaking imports into finely divided categories and applying a number of controls. Their conclusion, however, matches what one gets from a quick-and-dirty overview: Foreign suppliers bore very little of the burden of tariffs. As you can from the data in the last column of the table below, the overwhelming share of the cost of the tariffs fell on Americans – either producers or consumers. Over time that share ranged from 94% to 86%.

s_!2mex!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Ffaf4273e-738d-4fad-9090-d0b88a6187ac_926x416.png){kind=link}

{kind=link}

. The gap between that forecast and actual inflation is about 0.8 percentage points, not far short of the extra 1 percent inflation conventional analysis would predict. Another way to gauge tariffs’ impact is to look at narrower measures of inflation that focus on the prices we expect tariffs to affect. The Trump tariffs apply only to physical goods as opposed to services. Some economists I highly respect like to look at [core goods inflation](https://x.com/ernietedeschi/status/2022343609698390516), which excludes food, energy, and also used cars. That measure of inflation jumped sharply after the Trump tariffs. s_!_kUS!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fde926989-c36a-494c-b830-ede1c0de3edd_1240x828.png](https://substackcdn.com/image/fetch/\(s_!6Sem!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F35e9ece6-ec61-47d8-9a50-10bc5f2ec546_1240x828.png)

Chart 6 Source: Bureau of Economic Analysis and Survey of Professional Forecasters

Unlike the Consumer Price Index, the PCE price index has not shown continuing disinflation. Before the Trump tariffs, most economists believed that inflation would continue to fall. The line in Chart 6 labeled “Projected” is the average prediction for inflation over the course of 2025 from the late 2024 [Survey of Professional Forecasters](https://www.philadelphiafed.org/-/media/FRBP/Assets/Surveys-And-Data/survey-of-professional-forecasters/2024/spfQ424.pdf). The gap between that forecast and actual inflation is about 0.8 percentage points, not far short of the extra 1 percent inflation conventional analysis would predict.

Another way to gauge tariffs’ impact is to look at narrower measures of inflation that focus on the prices we expect tariffs to affect. The Trump tariffs apply only to physical goods as opposed to services. Some economists I highly respect like to look at [core goods inflation](https://x.com/ernietedeschi/status/2022343609698390516), which excludes food, energy, and also used cars. That measure of inflation jumped sharply after the Trump tariffs.

s_!_kUS!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fde926989-c36a-494c-b830-ede1c0de3edd_1240x828.png){kind=link}

{kind=link}

Write a comment